"Expected 40 Trillion, Got 37 Trillion"... First 'Hold' Rating on SK Hynix Emerges

BNK Securities issues lone downgrade... "Late-stage AI cycle, HBM4 margin dilution, weakening H2 momentum"

- BNK Securities downgraded SK Hynix from Buy to Hold after Q1 profit missed expectations

- Late-cycle AI risks and HBM4 margin pressure drove the first domestic brokerage downgrade

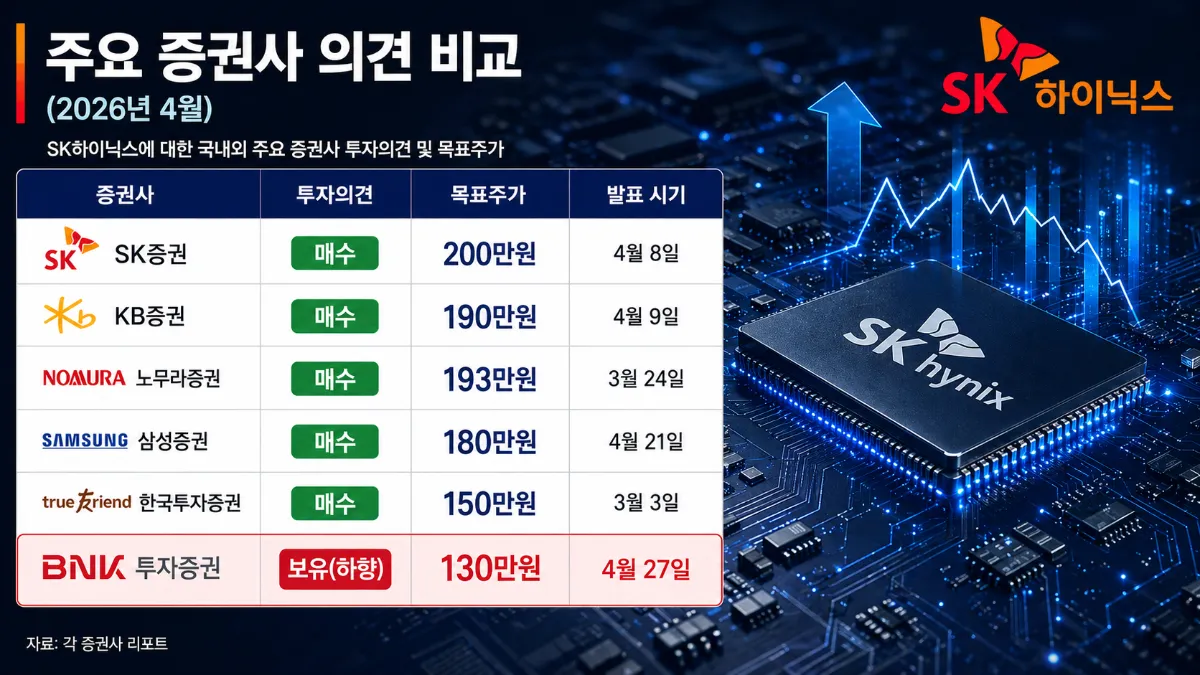

For the first time, a brokerage has issued a downgrade opinion on SK Hynix (000660). This contrarian view emerges amid a broader market sentiment where multiple securities firms have raised target prices to the 2 million won range while recommending buy ratings.

BNK Securities downgraded SK Hynix from 'Buy' to 'Hold' on the 27th, while maintaining its target price of 1.3 million won.

① "Failed to Meet 40 Trillion Expectations"

BNK Securities analyst Lee Min-hee noted that SK Hynix's Q1 results failed to meet market expectations of over 40 trillion won in operating profit following Micron and Samsung Electronics' earnings announcements. SK Hynix's Q1 consolidated operating profit, disclosed on the 23rd, reached 37.61 trillion won, up 405.5% year-over-year but falling short of some market expectations.

② "AI Inference Cycle Entering Late Stage"

The analyst diagnosed that the AI inference cycle that began last year has entered its late stage. Hyperscalers' upward trend in AI capex has been slowing since March, and the gap between spot and fixed contract prices is also narrowing.

While supply-demand dynamics remain tight in H2 due to existing large server orders, momentum itself is expected to decelerate. The analyst stated, "Despite steep earnings growth, considering entry into the late cycle stage and weakening H2 momentum, the stock is now expected to transition to a low P/E cyclical play."

③ "Higher HBM4 Mix Pressures Margins"

Another reason for H2 deceleration is the expanding sales mix of 6th-generation High Bandwidth Memory (HBM4). HBM4's higher technical complexity compared to HBM3E requires more time for initial production costs and yield stabilization. While unit prices are higher, initial margins may be lower, creating a burden on short-term profitability as HBM4's sales proportion rapidly increases.

④ "Potential Revaluation as Low P/E Cyclical Stock"

The analyst noted "the possibility of valuation transition from high-growth premium to low P/E cyclical stock." As growth momentum decelerates, the market begins trading at lower multiples aligned with actual profit levels.

Currently, most securities firms maintain buy ratings on SK Hynix with target prices ranging from 1.8-2.1 million won. BNK Securities' downgrade represents the only hold rating among domestic brokerages, significantly diverging from market consensus.

AI Summary

BNK Securities downgraded SK Hynix from Buy to Hold. Q1 operating profit of 37.6 trillion won fell short of 40 trillion won expectations, with late-stage AI cycle, HBM4 margin dilution, and hyperscaler investment slowdown acting as combined headwinds. This marks the first downgrade among brokerages while most maintain buy ratings around 2 million won.

Frequently Asked Questions

Q. Why does HBM4 reduce profitability?

HBM4's higher technical complexity requires more time for initial production costs and yield stabilization. While unit prices are higher, initial margins may be lower, creating pressure on short-term profitability as the mix rapidly increases.

Q. What are other brokerages' views on SK Hynix?

Most maintain buy ratings with target prices of 1.8-2.1 million won. BNK Securities' hold rating is currently the only one among domestic brokerages.

Q. What's the impact of transitioning to a low P/E stock?

When growth premiums disappear, share prices get revalued to align with actual profit levels. This means limited upside potential even as earnings grow.

Related Stocks & ETFs

Direct Exposure: SK Hynix (000660), Samsung Electronics (005930), Micron (MU)

HBM Supply Chain: Hanmi Semiconductor (042700), TSMC (TSM), NVIDIA (NVDA)

ETFs: KODEX Semiconductor (091160), TIGER Semiconductor (091230), iShares SOXX (SOXX), VanEck SMH (SMH)

Frequently Asked Questions

BNK투자증권이 SK하이닉스 투자의견을 하향한 이유는 무엇인가요?

1분기 영업이익 37.6조 원이 시장 기대치 40조 원에 미달했고, AI 추론 사이클이 후반부에 접어들었으며, HBM4 초기 마진 부담과 하이퍼스케일러 투자 둔화 등이 복합적으로 작용했기 때문입니다.

HBM4가 수익성을 떨어뜨리는 이유는 무엇인가요?

HBM4는 기술 난이도가 높아 초기 생산 비용과 수율 안정화에 시간이 더 걸립니다. 단가는 높지만 초기 마진은 낮을 수 있어 비중이 빠르게 늘수록 단기 수익성에 부담이 됩니다.

다른 증권사들의 SK하이닉스 의견은 어떤가요?

대다수는 목표주가 180만~210만 원의 매수 의견을 유지하고 있습니다. BNK투자증권의 보유 의견은 현재까지 국내 증권사 중 유일합니다.

저 PER주 전환이 주가에 미치는 영향은?

성장 프리미엄이 사라지면 주가가 실제 이익 수준에 맞게 재평가됩니다. 이익이 늘어도 주가 상승 여력이 제한될 수 있다는 뜻입니다.

하반기 SK하이닉스 실적 전망은 어떤가요?

기존 서버 주문으로 수급은 타이트하지만, AI 사이클 후반 진입과 하이퍼스케일러 투자 증가세 둔화로 성장 모멘텀은 완만해질 것으로 전망됩니다.

Microsoft Eyes DeepSeek V4 for Copilot Cowork, Squeezing Out OpenAI and Anthropic on Cost

Nvidia's 85% Revenue Surge Still Couldn't Lift the Stock — A Textbook 'Sell the News' Event

Nokia Surges 140% YTD — Nvidia's $1B Bet Rebrands It as an AI Infrastructure Play

Wall Street's Defining Moments

See more

Smart Money Briefing

Weekly summaries of Wall Street guru moves and crypto whale activity.